Lose Your Group Health Insurance Plan?

HERE’S HOW TO FIND NEW COVERAGE

The coronavirus pandemic has left many individuals and families without employer-sponsored health insurance due to an involuntary job loss or reduction in work hours. During this challenging time, it is important to avoid a lapse in coverage that could leave you vulnerable to catastrophic healthcare costs or subject to a state financial penalty. Here are some tips on how and when to apply for new coverage.

First, if your spouse or domestic partner has a job that provides health insurance, you may be eligible for coverage under their plan. If you’re younger than age 26, you may be able to join your parent’s group health insurance plan as allowed by the Affordable Care Act (ACA). With these options, you have only 30 days from the time your previous employer stops paying for your insurance to enroll in a plan.

If your annual income is reduced due to a job loss or another reason, you may also be eligible for Medi-Cal, which is California’s Medicaid plan. Medi-Cal provides free or low-cost health insurance primarily for low-income families and children, pregnant women, the elderly and people with disabilities. Since eligibility is mainly based on current household monthly income, a job loss may serve as a qualifying event for enrollment. In 2021, the Medi-Cal income limit for an individual is $17,775 and $36,570 for a family of four.

For most Americans, there are two main paths to obtain health insurance after an involuntary loss of job-based health insurance coverage. The first option is through the Consolidated Omnibus Budget Reconciliation Act (COBRA), a program that extends your current health insurance plan for up to 18 months after your employment is terminated. The second option is through the state’s health insurance marketplace, Covered California, which qualifies you for a special enrollment period.

Is COBRA Right for You?

You have the legal right to continue on your former company’s group health insurance plan for a set period of time after a job loss through COBRA. Typically, employers with at least 20 full-time employees are required to offer COBRA coverage. It is generally available to former employees and retirees, as well as to their spouses, former spouses and dependent children if they were originally covered.

However, this option can be cost-prohibitive because you are responsible for paying both your portion and your employer’s portion of the premium plus a 2 percent administrative fee – causing your premium to dramatically increase. You normally have 60 days to enroll once you receive the COBRA notice. Even if you initially waive coverage, you remain eligible to enroll within the 60-day window. Once you opt into COBRA, you cannot switch to a plan through a health insurance marketplace until open enrollment begins in November or until COBRA ends in 18 months.

While the federal government fully subsidized COBRA premiums for six months beginning in April 2021 as part of a COVID-19 stimulus relief package, this provision expired on September 30, 2021.

Shop for a New Plan at Covered California

If COBRA proves too expensive, you can also enroll for coverage through the state’s own marketplace called Covered California. This service connects California residents with brand-name health insurance companies such as Anthem, Blue Shield, Kaiser, Health Net and more.

Consumers can sign up now to benefit from the increased financial help provided by the American Rescue Plan (ARP), which will continue to provide lower premiums at unprecedented levels throughout the entire 2022 coverage year. The ARP is already lowering premiums for an estimated 1.5 million Californians, and thousands more could get help becoming insured or reducing the cost of the coverage they have now.

This federal law ensures that everyone eligible will pay no more than 8.5 percent of their household income on their health plan premiums if they enroll through an ACA marketplace. The latest data shows that nearly 700,000 people enrolled in Covered California now have quality coverage from quality health plans for only $1 per month.

For example, the ARP lowered the average premium cost by 50 percent for many Californian households that were already eligible for financial help, and newly eligible middle-income families are saving an average of more than $400 per month. With 12 carriers providing coverage across the state in 2022, all Californians will have two or more choices, 94 percent will be able to choose from three carriers or more, and 81 percent will have four or more choices.

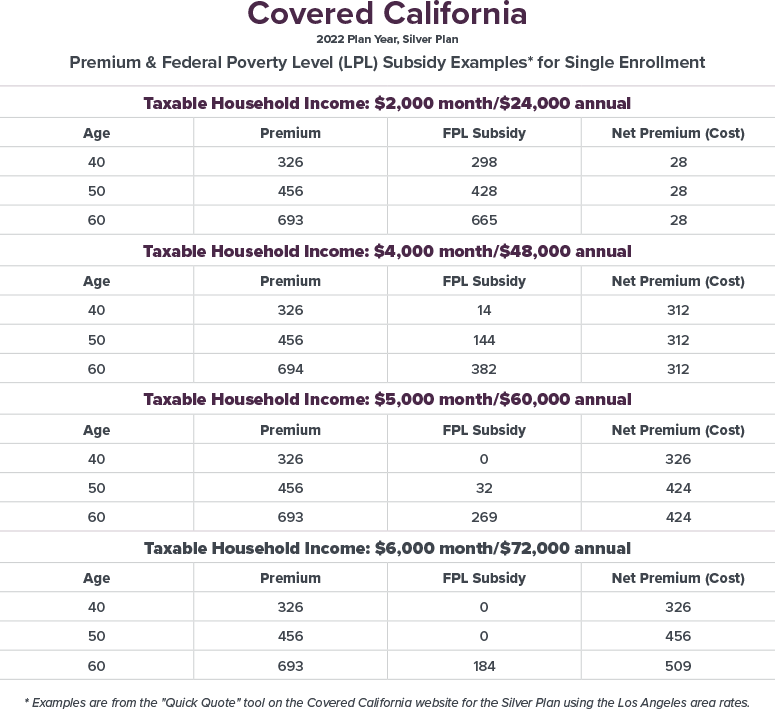

The ARP lowered net premiums across households in 2021. The subsidy was continued for 2022. The table below demonstrates the net premiums paid by a single individual, in the Los Angeles area, enrolling in the Silver Plan. This coverage option is the most popular of the plans offered by Covered California.

The combination of expanded financial help, increased competition and consumer choice have contributed to record enrollment in Covered California, which gives the state one of the healthiest consumer pools in the nation for the seventh consecutive year. These were also key factors in negotiating a preliminary rate increase for California’s individual market of just 1.8 percent in 2022, and a three-year average of only 1.1 percent from 2020-2022.

The latest rates and choice of carriers will go into effect Jan. 1, 2022. Consumers do not need to wait for the traditional open-enrollment period in November to sign up for coverage. Covered California opened a special-enrollment period to allow the uninsured, and those enrolled directly through a health insurance carrier, to sign up for a plan through Dec. 31, 2022 and benefit from the extra financial assistance made available by the ARP.

Where to Find Enrollment Assistance

To find out if you are eligible for Covered California or Medi-Cal, whether you qualify for financial help and which plans are available in your area, visit Covered California. You can learn more about your coverage options by using the Covered California “Shop and Compare Tool” and entering your ZIP code, household income and the ages of those who need coverage.

You may also get free and confidential assistance over the phone, in a variety of languages, from Covered California by calling (800) 300-1506. A certified enroller can provide assistance with:

Determining coverage eligibility for Medi-Cal or Covered California

Providing an estimate of the eligible credit (maximum cost) for coverage

Processing the enrollment for either Medi-Cal or Covered California

If you wish to speak with a Medi-Cal enrollment support specialist directly, you may call (888) 663-8289 for information on L.A. Care, the free or low-cost health care program that provides access to medical services for eligible Los Angeles County residents.

Losing employer-sponsored health coverage can be a stressful life event for you and your family. However, there are many options to find a new insurance plan that provides peace of mind and best serves your medical needs.